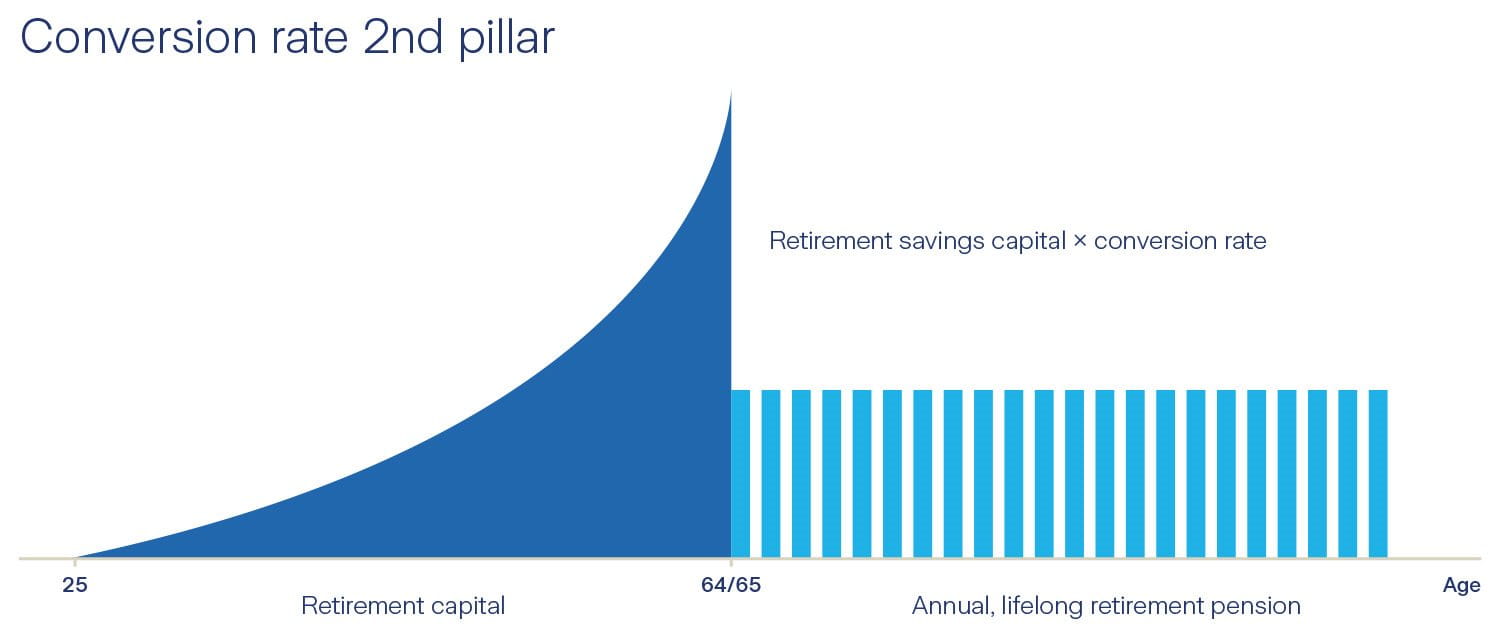

The conversion rate is coming under increasing pressure: On the one hand, due to increasing life expectancy, and on the other hand, due to falling investment returns. Nevertheless, the statutory minimum conversion rate was gradually reduced between 2006 and 2014 with the BVG revision (2005) from its original level of 7.2% to the current 6.8%.

However, what is often overlooked is that a lower conversion rate does not automatically lead to lower pensions. A reduction in the conversion rate minimizes the redistribution from active insured persons to pension recipients and thus creates more scope for higher returns on pension capital. At Vita Invest, four additional retirement pensions could be paid out with a conversion rate of 4.3%. It is therefore important to consider the conversion rate in the overall context of pension benefits and investments in order to ensure stable and sustainable pensions in the long term.